Get up to $10,000 in credit using your car

Get a credit card using your car as collateral. Keep driving while building credit.

Unlimited 1.5% cashback rewards

Check your offer in under 1 minute

No cash deposit required

A better way to borrow with your car

Keep your car. Use it as collateral.

No hidden fees or sky-high interest

Revolving credit line, not a one-time loan

Use your card before it even arrives

How Yendo compares to a traditional collateral loan

Keep and drive your car

May require surrendering your vehicle until repaid

Revolving credit line with a Mastercard credit card

One-time lump sum with strict repayment terms

Fixed APR, no hidden fees

Rates can exceed 100% APR, fees vary and are often predatory¹

Monthly payments, spend as needed

Rigid repayment schedule, often within 30 days²

Online pre-approval decision

In-person or phone, slower approval times

Your Yendo Credit Card is just 3 steps away

See why our customers love us!

"Yendo was quick and easy.I recommend Yendo to anyone who will listen. I'd say at least try the process. You'd be very happy.”*

"If you're looking for that credit that you've not been able to come up with, Yendo is probably exactly what you're looking for."*

"I heard about Yendo through a friend from the start through the application process, through the funding was very quick and very pain free."*

Build credit with responsible usage and repayment

FAQs

With responsible usage, Yendo can help build your credit. We report to Experian, Equifax and TransUnion.

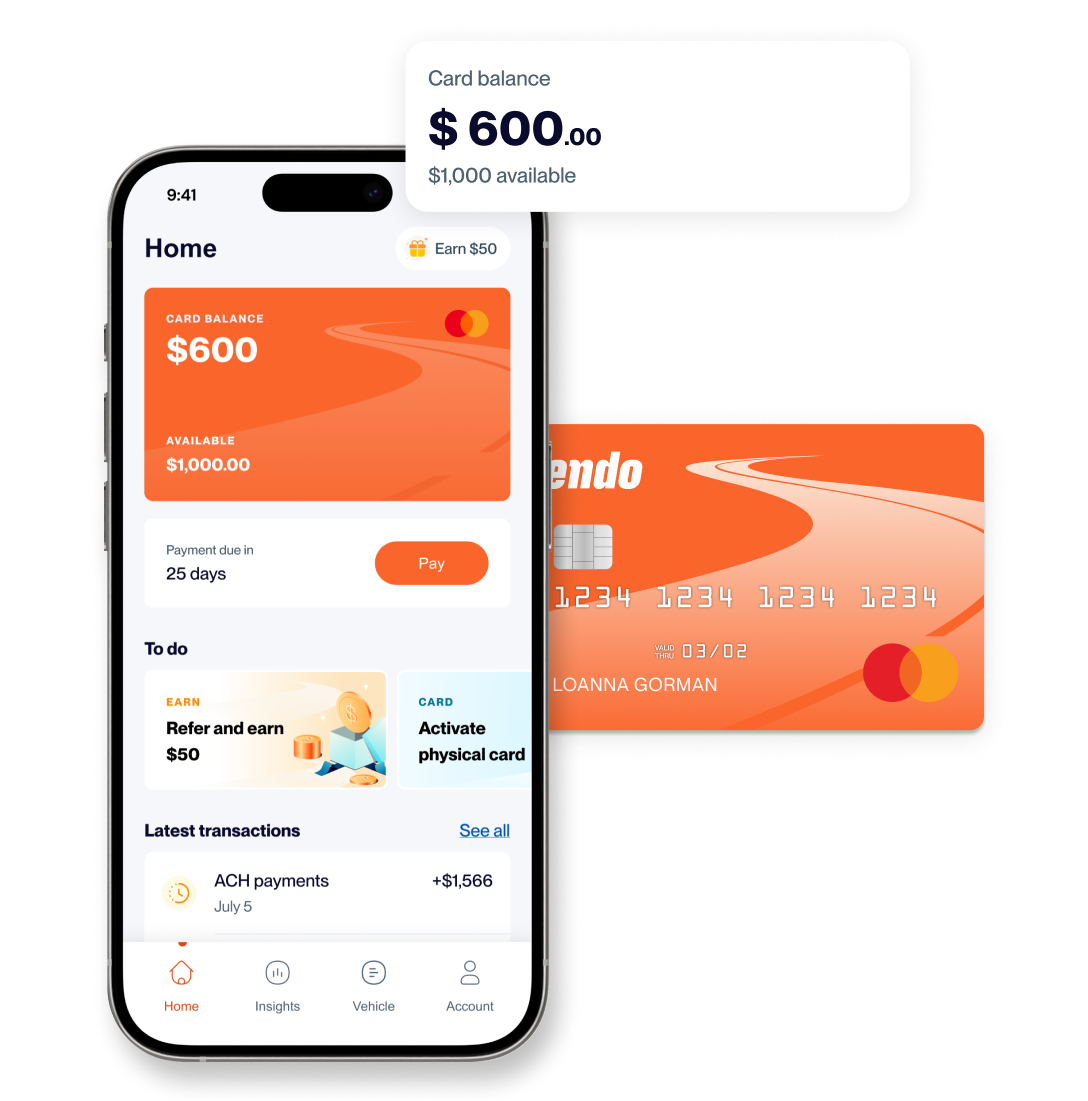

Yendo Credit Cards have credit limits ranging from $450 up to $10,000. Your credit line depends on the make, model, mileage, and condition of your vehicle, credit history, in addition to your ability to repay.

You have 25 days after the end of your monthly statement to make a payment. You can make payments at anytime, and you will need to make a minimum payment of 1% of your statement balance + interest and fees. We're here to help, so if you do need assistance making your minimum monthly payment, please give us a call.

You can get approved as long as you meet Yendo’s other approval criteria. Our mission is to offer affordable credit access to everyone.

Most Yendo cardholders have access to their virtual credit card within an hour of completing their application and mailing their title if required. The virtual card can be used online or with Apple, Google, or Samsung pay. A physical card will be mailed to you and typically arrives in 3-7 days.

We will always work with you to try to establish a plan that works with your situation. However, as a lienholder, we can exercise our right to recover an outstanding balance, but this is our last option. Keep in mind that with Yendo, your minimum monthly payment can be more affordable compared to other alternatives like title loans.

You can get your title back at any time by paying off your balance and giving us a call to close your account. Once we verify that your balance is $0, Yendo will close your account and remove its lien from your title. We will then release the title to you within 10 days of payoff - please note that there may be some situations outside of Yendo's control, such as DMV processing timelines, that could extend this timeframe. Or you can keep your account open with a $0 balance and pay no interest, so you can have continued access to your credit card when or if you wish to use it.

While your official due date is 25 days after receipt of your previous monthly statement, you can pay off all or a portion of your balance in advance at any time. The best part? If you pay your statement balance on or before the due date every month, you’ll pay zero interest on purchases. In the event you don’t pay off your full balance, our minimum payment is 1% of your principal balance or $50, whichever is greater. Please note if you have interest or fees charged to your account, these will be added to your minimum payment due.

If your balance exceeds your credit limit, your account is overlimit. You will need to make a payment that brings your balance below your credit limit and make at least a minimum payment to unblock your card.