Smart Money

How Do Title Loans Work in California? | Yendo Credit Card

Cory

June 16, 2023

|

5

min read

Are title loans legal in California?

Title loans are legal in California, but they are subject to specific regulations and restrictions and are generally associated with high interest rates, as high as 291%.

A title loan is a short-term, high-interest loan that uses the borrower's vehicle title as collateral. In California, lenders offering title loans must be licensed by the California Department of Financial Protection and Innovation (DFPI).

Title loans in the news:

How title loans work in California

- Application process: The borrower provides their vehicle details and paperwork, such as the vehicle's title, proof of insurance, valid government-issued ID, and proof of income. The lender evaluates the vehicle's value and condition to determine the loan amount they are willing to offer.

- Loan terms and fees: If the borrower agrees to the offered loan amount, the lender presents the loan terms, interest rates, and fees applicable to the loan. California regulates the interest rates for title loans based on the loan amount.

- Lien on the vehicle: Once the borrower agrees to the terms and signs the loan agreement, the lender places a lien on the vehicle's title. The borrower can continue using their vehicle during the loan term.

- Repayment: The borrower must repay the loan, including the principal amount, interest, and any fees according to the agreed-upon repayment schedule, which can be as short as 30 days or extended over several months.

- Loan default: If the borrower fails to repay the loan as agreed, the lender has the right to repossess and sell the vehicle to recover the debt, often without providing a notice of repossession.

Although title loans are legal in California, they are associated with high interest rates and short repayment terms, which can lead borrowers into a cycle of debt and risk of vehicle repossession. It's essential to explore alternative financing options before considering a title loan. These could include personal loans, credit cards, or borrowing from friends and family. If a title loan is necessary, be sure to only borrow what you can afford to repay and carefully review the loan terms and conditions.

Where can I find resources on title loans on California?

To find the most accurate and up-to-date information on title loan laws in California, you can refer to the official state legislative and regulatory sources:

- California Department of Financial Protection and Innovation (DFPI) - The DFPI supervises and regulates title loan companies and other financial services providers in California. Their website provides information on license requirements, consumer protections, and applicable regulations. Link: https://dfpi.ca.gov

- California Financial Code - Title loans in California are primarily governed by the California Financial Code, Division 1.2, covering "Finance Lenders and Brokers." The code outlines regulations and rules for lending practices, interest rates, and licensing requirements. Link to the code: https://leginfo.legislature.ca.gov/faces/codes_displayText.xhtml?division=1.2.&lawCode=FIN&title=&part=4.&chapter=&article=

- California Civil Code - The California Civil Code also contains provisions affecting title loans, including regulations on the repossession and sale of collateral in specific situations. Link to the code: https://leginfo.legislature.ca.gov/faces/codes_displayText.xhtml?lawCode=CIV&division=3.&title=14.&part=4.&chapter=9.&article=

For a comprehensive understanding of title loan laws in California, it is advisable to consult these sources and potentially seek legal advice if you require further clarification on specific aspects or issues related to title loans.

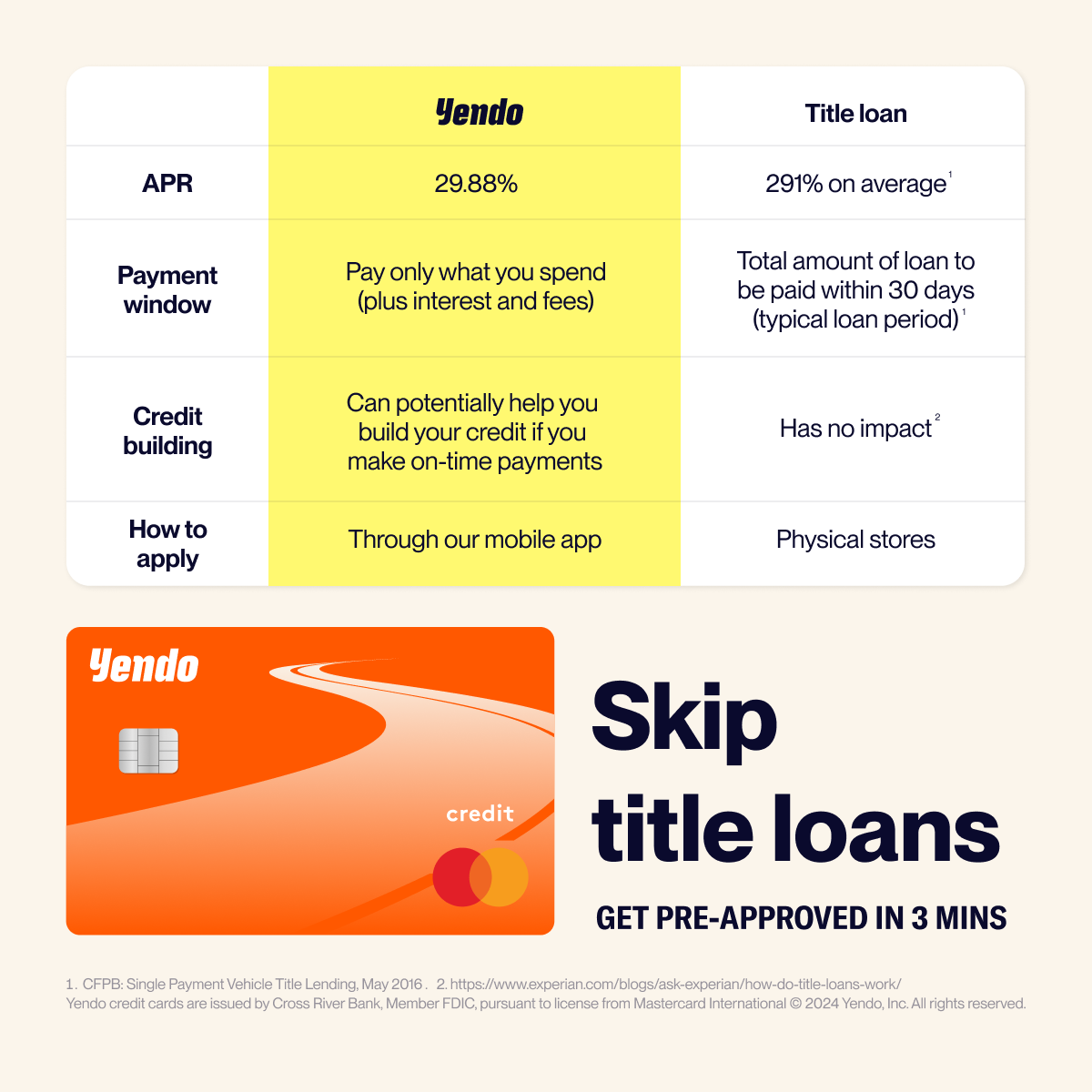

The Yendo Card - The Title Loan Alternative

Yendo is the first credit card that's backed by the value of your car, so you can use your car title to get a credit line of up to $10k.

The card can provide access to credit for those who might not be able to qualify for other credit cards. It's a real credit card, powered by Mastercard, that provides credit limits from $450 - $10,000, depending on the value of your car.

So, rather than re-applying for loans, for example, you can access funds an ongoing basis and, with responsible usage like on-time payments, build your credit too.

Compare Yendo versus a Title Loan

Looking to access funds quickly, at a significantly lower cost to you versus a title loan? Apply for Yendo, here's why:

Features & benefits of the card

- Credit limit - access up to $10k in credit

- Only pay for what you spend - it's a credit card, so you only pay for what you spend, plus interest and fees. Or, if you pay off your balance each month, you only pay for what you spend.

- App - the Yendo app lets you manage your account, wherever you are

- Virtual card - access a portion of your credit limit prior to getting your physical card in the mail with the Yendo virtual card. Use your virtual card in addition to your physical card

- Cash advances - ability to do cash advances on your card if you need to access money quickly

- Access to revolving credit – you’ll have a revolving line of credit that opens up as you make payments

- Credit reporting – all your account activity will be reported to the credit bureaus, giving you the perfect opportunity to build your credit

Additional information

- CFPB Orders TitleMax to Pay a $10 Million Penalty for Unlawful Title Loans and Overcharging Military Families

- Title loans 101

- Yendo Los Angeles

Disclaimer: Yendo is not a provider of financial advice. The material presented on this page constitutes general consumer information and should not be regarded as legal, financial, or regulatory guidance. While this content may contain references to third-party resources or materials, Yendo does not guarantee the accuracy or endorse these external sources.